Self-paced

Economist: Support Currently the interest rates that banks pay to borrow are higher than the interest rates that they can receive for loans to large, financially strong companies. █████ ████ ███ █████████ ████ ██ █████████ ████ ███ ███ ███████████ ███████ ███ █████ ███████ ██ █████ ██ █████ ███ ████████████ █████████ ██ ████ ████ ██ ███ ████ █████ ████ ██ █████ ████ ███████ ██ █████████ ██ ████ ████ ██ ███ ████ █████ ████

Four Kinds Of Companies

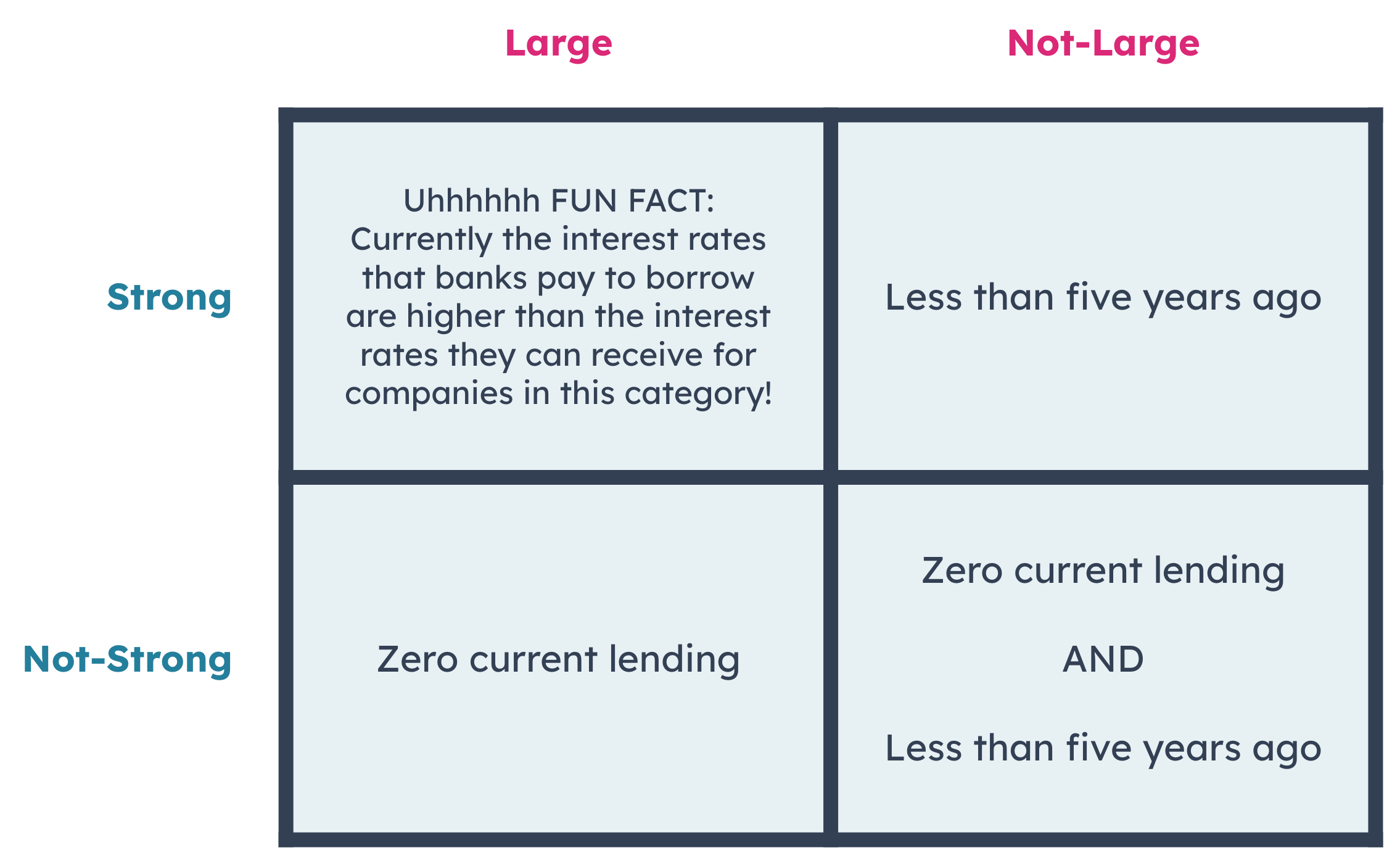

The economist’s conclusion is that total lending across all companies is less today than it was five years ago. In support, the economist splits companies up into four categories, and gives us information about each of those categories. For the most part, that information is great and supports the conclusion quite well. For one of the categories, though (spoiler alert: it’s Large-and-Strong companies), the information isn’t relevant to the conclusion unless we make an assumption.

We’re gonna think about the supporting premises using a 2 x 2 table. Within the economist’s argument, companies are either Strong or Not-Strong, and they’re either Large or Not-Large (i.e. small-or-medium). Here’s how the premises map onto that structure:

Let’s start with the bottom row, where the economist tells us

Those claims cover three of our four categories, and we can comfortably say that lending to companies in those categories is less today than it was five years ago.

But what about companies that are Large-and-Strong? If lending to Large-and-Strong companies skyrocketed over the past five years, the economist’s conclusion about total lending is screwed.

The economist doesn’t give us any direct information about how much banks are lending to Large-and-Strong companies. Instead, we’re just given a fun fact: “currently the interest rates [blah blah blah].”

So that’s what’s missing. For the economist’s argument to work, we need actual information about how much banks are lending to Large-and-Strong companies. Phrasing this as a sufficient assumption, we get:

[That fun fact about interest rates] means banks are not currently lending more to Large-and-Strong companies than they were five years ago.

21.

The economist's conclusion follows logically ██ █████ ███ ██ ███ █████████ ██ ████████

a

Banks will not ████ █████ ██ ████████ █████ ████ ███ █████ ████ ███ ████████ █████ ████ ███ ██ ███████

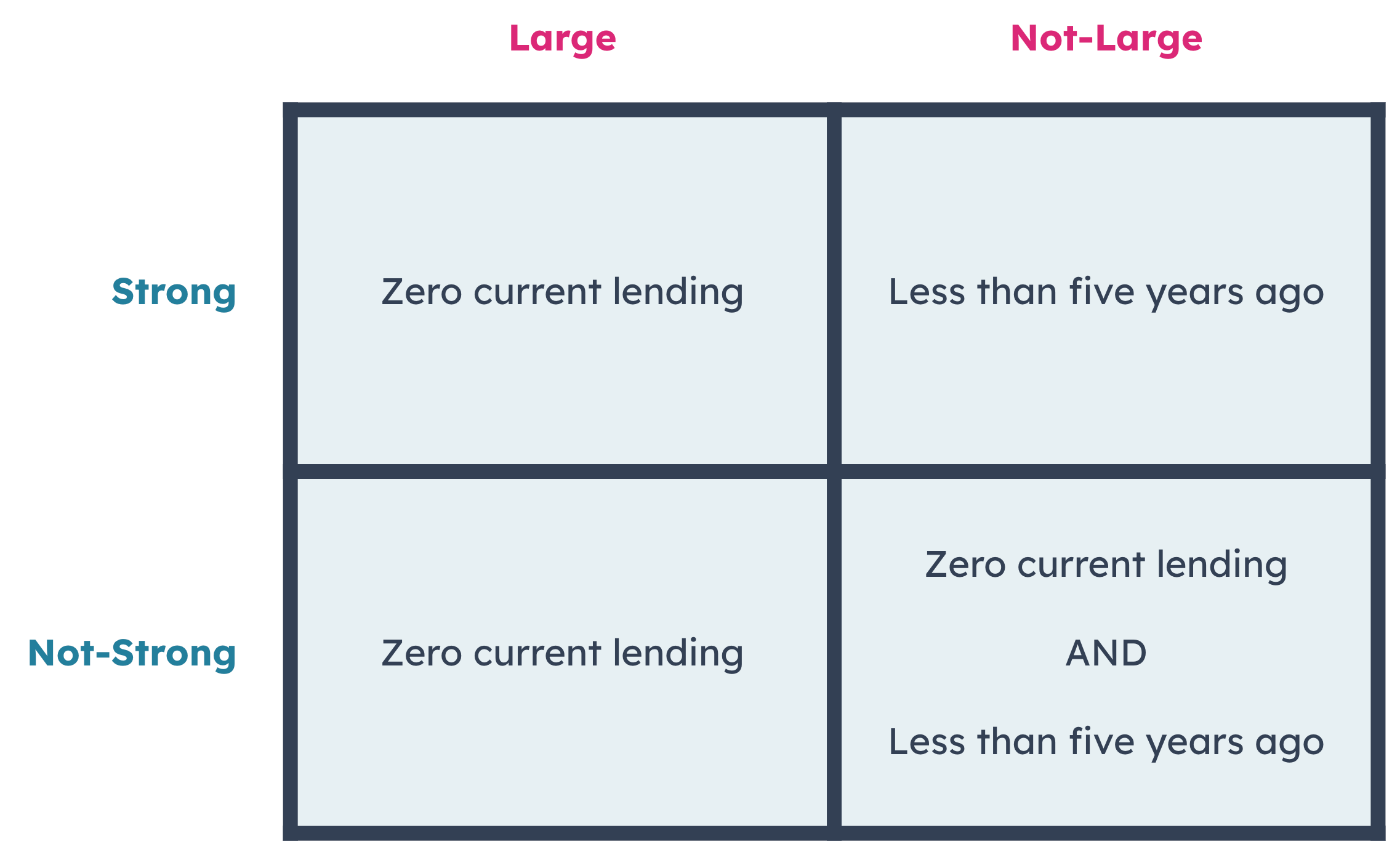

This fills in the missing information about Large and Strong companies in the economist’s argument. The other premises establish that bank lending to the other three kinds of companies (Not-Large and Strong; Large and Not-Strong; Not-Large and Not-Strong) is less than it was five years ago. See the 2 x 2 in the analysis section for more detail on that.

To reach a conclusion about total lending, the economist needs to connect

(A) essentially says “if [that fun fact I mentioned earlier] is true for a company, banks will not lend any money to that company.” That tells us banks are currently lending nothing to Large-and-Strong companies, which completes the support structure for the conclusion about total lending across all companies:

b

Most small and ████████████ █████████ ████ ███████████ ████████ ████ █████ ███ ████ ████ ███ ████

The economist’s argument is missing information about how much banks are currently lending to companies that are Large-and-Strong, which (B) doesn’t provide.

(B) provides some more color about Not-Large companies, but we already know the thing that matters – they’re receiving less lending now than they were five years ago.

c

Five years ago, ████ █████ █████ ████ ██ █████████ ████ ████ ███ ███████████ ███████

The economist’s argument is missing information about how much banks are currently lending to companies that are Large-and-Strong, which (C) doesn’t provide.

(C) tells us that five years ago, the lending numbers for Not-Strong companies were greater than zero. That’s nice, because it solidifies that these companies are indeed receiving less lending than they used to be (since zero is less than more-than-zero). But it still doesn’t repair the major hole in the argument.

d

The interest rates ████ █████ █████████ ███ ██ ██████ ███ ██████ ████ ███ █████ ████ ████ ████ █████ ████

This suffers from the same flaw as the original argument – there’s no established connection between the interest rates banks pay to borrow money and their willingness to lend money. Without that link, we can’t make any conclusions about total lending patterns.

e

The interest rates ████ █████ ███ ████████████ █████████ ███ ██ ██████ ███ ██████ ████ █████ ████ ██ ██████ ███████████ ██████ ██████████

The economist’s argument is missing information about how much banks are currently lending to companies that are Large-and-Strong, which (E) doesn’t provide.

On a structural level, (E) is missing the same thing as the original argument – there’s no established connection between interest rates and banks’ willingness to lend money. Without that link, we can’t make any conclusions about total lending patterns.